The MDL mirrors the EUR volatility: Moldovan economy adjusts to new reality

Commentary by InfoMarket

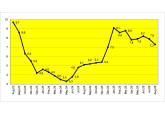

Since the EUR became the base currency of the National Bank of Moldova (NBM) for determining the exchange rate of the MDL and conducting currency interventions (January 2, 2025), the country's national currency has depreciated by 5.58%.

When the national currency was introduced in Moldova on December 29, 1993, the USD was the base currency for determining the exchange rate. The exchange rates of other currencies were determined through cross rates. The USD was also used in the NBM's calculations, currency interventions, and other instruments, calculations, and reports. Thirty-one years after the introduction of the national currency in Moldova, the NBM decided to change the base currency from the USD to the EUR.

The transition took place on January 2, 2025. On that day, the EUR exchange rate was MDL 19.1559. Fourteen months later, on March 2, 2026, it was MDL 20.2257. During this period, the MDL devalued by 1.07 lei, or 5.58%.

The NBM's decision to switch to the EUR as the base currency was more structural than opportunistic. It reflects changes in the country's trade geography and financial flows. More than 60% of Moldova's foreign trade turnover is with European Union countries, a significant part of remittances comes from the eurozone, and the European currency is increasingly used in contracts between importers and exporters.

However, along with this logic, the MDL has actually become more sensitive to the dynamics of the EUR on world markets. Whereas previously the USD was the main benchmark for business and regulators, now the daily exchange rate architecture is built around the European currency. This means that fluctuations in the EUR/USD pair, decisions by the European Central Bank, and global capital flows are increasingly reflected in the official exchange rate in Moldova and in the behavior of market participants.

However, it is important to understand that a 5.58% devaluation over 14 months does not appear to be a crisis. For a small open economy such as Moldova's, this is more of a moderate adjustment. The question is whether it will mark the beginning of a trend or remain an adaptation to the new currency base.

In the coming months, the dynamics of the MDL will depend on a combination of internal and external factors. Domestically, the balance of payments remains key. If imports continue to outpace exports, demand for currency will remain high. On the other hand, transfers from the eurozone, European financing, and grant support form the supply of euros on the market and smooth out the pressure.

Externally, the decisive factor is the global dynamics of two currencies: the EUR and the USD. Despite the change in the base currency, Moldova's energy and raw material imports are still largely denominated in US dollars. This means that not only the MDL/EUR exchange rate is critical for inflation, but also the MDL/USD exchange rate (already through the cross rate), as well as global oil and fuel prices.

Geopolitical instability in the Middle East, including escalation in Iran, is adding to market jitters. Any risks to oil supplies are factored into rising prices, which strengthens the USD and increases the cost of energy resources. In this case, pressure on prices in Moldova is increasing even with a relatively stable MDL/EUR exchange rate.

The devaluation of the MDL is putting pressure on inflation. With moderate devaluation and stable external prices, the impact could add 0.8-1.2 percentage points to the annual inflation rate. For goods (food, appliances, medicines, building materials, etc.) settled in euros, the weakening of the MDL will increase the purchase cost for importers when converted into national currency. For energy resources, the primary factors are the USD and the global price of oil, which has been on an upward trend against the backdrop of events in the Middle East.

But the most significant risk for Moldova is possible inflationary expectations. If businesses start to price in a further weakening of the MDL in advance, there will be a secondary effect. It is this factor that will determine whether inflation will exceed the target range or remain within it. And in a situation where currency pressure and rising oil prices coincide, the impact of the MDL's devaluation on the inflation rate may intensify.

In such a situation, the NBM faces a classic dilemma. Raising the base rate can curb inflation expectations, make the MDL more attractive for savings, and cool excess demand. However, the rate cannot directly influence global oil prices or geopolitical risks. Too sharp a tightening could slow down lending and economic activity without any guarantee of neutralizing the external shock.

In the baseline scenario, with the inflow of European funding continuing and no sharp jump in commodity prices, the MDL will fluctuate within a manageable range and inflation will remain within the target corridor. In a stress scenario—with rising oil prices, a strengthening USD, and a deteriorating trade balance—pressure on prices will intensify, and the NBM will have to respond with tighter monetary policy. In an optimistic scenario, the stabilization of global markets and export growth will offset currency pressure without the need for a significant rate hike.

Thus, the transition to the EUR as the base currency has changed the structure of exchange rate risks, but has not eliminated the fundamental patterns: the MDL exchange rate is still determined by the state of foreign trade, capital movements, and the global economic situation. In 2026, it is the combination of these factors, rather than the change in the currency base itself, that will be the main test for the country's inflation stability. //04.03.2026 - InfoMarket.