Banks as the fulcrum of the economy: they have increased profits and are preparing for the challenges of the 2H 2022

Commentary by InfoMarket Agency

It so happened that Moldova’s banking system is one of the most developed sector in terms of corporate management and addressing rapid changes of the situation and actions. There are 11 banks in our country, which are, first of all, commercial, which means that their task is to generate profit for the shareholders. In 2022, only one bank in Moldova remains fully controlled by Moldovan investors (Fincombank), while the rest are owned by foreign shareholders.

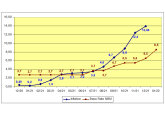

The banking 1H 2022 was significantly more profitable for market participants than 1H 2021 (the first post-Covid-19 year). Although, to be fair, it’s notable that banks managed to remain profitable in 2020 as well, even in the midst of the pandemic. Banks managed to remain profitable even though many "insure risks" during the crisis by allocating most of their profits to risk funds. This is due to the negative economic outlook in 2H 2022.

Every month InfoMarket Agency collects information from commercial banks on their activities: https://infomarket.md/en/databank/

From the table below, featuring data as of 30 June 2022, we can make some derivative calculations that will give a better understanding of how the country's banking sector performed in the first half of the year and perhaps assess projections for the second half of the year.

Bank profits as of 30 June 2022 compared to June 30, 2021

| Bank Name | Profit as of 30 June 2022 | Profit as of 30 June 2021 | Profit Ratio 30 June 2022 to 30 June 2021 (MDL) | Profit Ratio 30 June 2022 to 30 June 2021 (%) |

| BCR Chisinau | 54714,6 | 4589,6 | 50125,0 | 1092,14 |

| Comertbank | 16425,7 | 8892,3 | 7533,4 | 84,72 |

| Energbank | 33977,4 | 22265,1 | 11712,3 | 52,60 |

| Eurocreditbank | 14900,6 | 6628,5 | 8272,1 | 124,80 |

| Eximbank | 52663,2 | 28361,7 | 24301,5 | 85,68 |

| Fincombank | 52472,8 | 29147,5 | 23325,3 | 80,03 |

| maib | 514216,4 | 274057,5 | 240158,9 | 87,63 |

| Moldindconbank | 444928,4 | 267241,7 | 177686,7 | 66,49 |

| OTP Bank | 79643,2 | 152958,4 | -73315,2 | -47,93 |

| ProCredit Bank | 70806,9 | 39843,6 | 30963,3 | 77,71 |

| Victoriabank | 294671,7 | 107749,9 | 186921,8 | 173,48 |

| Total | 1629420,9 | 941735,8 | 687685,1 | 73,02 |

BCR Chisinau registered the largest increase in profit - up almost 12 times! But the profit of OTP Bank decreased almost twice. The first, as we know, earned on government bonds, the second - decided to increase prudential stability. But more about that will follow below.

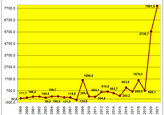

The 73% growth of profit in the banking system is due to two main factors: an increase in lending rates on loans and an increase in yields on government securities, where commercial banks are the main investors.

Loan (deposit) rates directly depend on the base rate set by the National Bank of Moldova (NBM). In the process of fighting inflation, the increase of the base rate is one of the NBM’s tools. Considering the situation and development forecasts, the NBM started to raise the rate in July 2021 (in November 2020 until July 2021 it was 2.65% per annum). Since then, the base rate has risen 9 times (of which 5 times in 2021). Since 3 June 2022, it has been 18.50% per annum.

That is, if in 1H 2021 the rate remained unchanged (2.65% per annum) then in 1H 2022 it rose from 6.50% to 18.5% per annum. This automatically led to a gradual growth of interest rates on loans in Moldovan lei (MDL) and, as a consequence, to an increase in bank revenues.

The yield that investors in government securities (GS) receive also depends on the base rate. According to the Ministry of Finance, in 1H 2021 the weighted average rate for all types of securities was 5% per annum, and in 1H 2022 - 14.71% per annum. At the last auction in June (14th) rates on government securities reached 19.50% per annum (for securities with maturity of 364 days). By the way, they keep growing - in July these securities (the most expensive) were sold at 19.89% APR. In general, until the growth of inflation is stopped (today it is 31.83% APR), it is hardly possible to say when stabilization and further reversal of dynamics will start.

Since in the current environment (especially based on the results of the first half of the year) banks are not looking at the second half of the year very brightly, many are strengthening their prudential policy, which is designed to prevent possible risks and problems in the activities of credit institutions. To put it simply, they increase risk funds from where they will cover possible losses if clients start to repay loans worse, thus maintaining the financial stability of the bank and good performance indicators. In the table on bank performance this column is called "Loan Impairment" - the indicator is rather complicated in internal calculations, but it is based on the risk fund. This is also where, as mentioned above, banks sometimes "hide" profits in order to be able to cover projected risks in the future.

Let us note the growth of loan portfolios of almost all commercial banks in 1H 2022 relative to the first half of 2021

| Bank Name | Loans as of 30 June 2022 (thousand MDL) | Loans as of 30 June 2021 (thousand MDL) | Dynamics of loans (MDL) | Dynamics of loans (%) |

| BCR Chisinau | 1093284,0 | 1006280,0 | 87004,0 | 11,57 |

| Comertbank | 971823,2 | 898950,1 | 72873,1 | 12,34 |

| Energbank | 979818,4 | 879923,4 | 99895,0 | 8,81 |

| Eurocreditbank | 668050,7 | 598852,0 | 69198,7 | 8,65 |

| Eximbank | 2241192,6 | 1777231,3 | 463961,3 | 3,83 |

| Fincombank | 1953183,1 | 1623513,8 | 329669,3 | 4,92 |

| maib | 20748889,7 | 16645301,5 | 4103588,2 | 4,06 |

| Moldindconbank | 11666804,6 | 9029295,6 | 2637509,0 | 3,42 |

| OTP Bank | 9236625,0 | 8168757,1 | 1067867,9 | 7,65 |

| ProCredit Bank | 3370278,1 | 3371862,2 | -1584,1 | -4,70 |

| Victoriabank | 5624973,9 | 4632558,9 | 992415,0 | 4,67 |

| Total | 58554923,3 | 48632525,9 | 9922397,4 | 4,90 |

The volume of lending decreased only for Procredit Bank, while all other banks recorded an increase, on average - by 4.9% in the system.

On the other hand, the Loan Impairment indicator does not depend on the volume of lending, but speaks only about the quality of the loan portfolio and, in today's situation, about the forecasted risks of a particular bank.

| Bank Name | Loan Impairment as of June 30, 2022 (thousand MDL) | Ratio "Loan Impairment" to "Loans" as of 30 June 2022 (%) | Loan Impairment as of 30 June 2021 (thousand MDL) | Ratio "Loan Impairment" to "loans" as of 30 June 2021 (%) | Difference in the share of "Loan Impairment" in "loans" in 1H 2022 to 1H 2021 (%) |

| BCR Chisinau | 41500,0 | 3,80 | 43069,1 | 4,28 | -0,48 |

| Comertbank | 12338,0 | 1,27 | 10397,0 | 1,16 | 0,11 |

| Energbank | 76813,3 | 7,84 | 53792,3 | 6,11 | 1,73 |

| Eurocreditbank | 7889,3 | 1,18 | 11353,3 | 1,90 | -0,71 |

| Eximbank | 111072,5 | 4,96 | 90588,4 | 5,10 | -0,14 |

| Fincombank | 59231,8 | 3,03 | 58604,7 | 3,61 | -0,58 |

| maib | 1064873,4 | 5,13 | 966971,6 | 5,81 | -0,68 |

| Moldindconbank | 619844,6 | 5,31 | 524098,0 | 5,80 | -0,49 |

| OTP Bank | 468433,9 | 5,07 | 294366,2 | 3,60 | 1,47 |

| ProCredit Bank | 109443,4 | 3,25 | 112950,6 | 3,35 | -0,10 |

| Victoriabank | 481051,0 | 8,55 | 410623,6 | 8,86 | -0,31 |

| Total | 3052491,2 | 5,21 | 2576814,8 | 5,30 | -0,09 |

Only three banks out of 11 increased their "risk funds" in 1H 2022 compared to 1H 2021. In a stable economic situation, this would indicate that most banks have improved the quality of the loan portfolio, while in those who have increased the "risk fund" the quality of the loan portfolio has deteriorated. However, in the present conditions it could also mean that the management of the banks increased their prudential risks in anticipation of deteriorating situation on the market.

Against this general background it is important to note a rather high liquidity of all commercial banks in Moldova. It is somewhat difficult to compare the indicators of the two halves of the year because last year "liquid assets" indicator was used in reporting, while starting this year instead of "liquid assets" indicator the LCR (Liquidity Coverage Ratio) indicator was introduced, which is calculated as a percentage. It is a liquidity indicator of a bank (enterprise), which reflects the degree of coverage of short-term payment obligations by current assets. That is, on the one hand, it should be at least more than 100%, and the higher it is, the higher is the liquidity of the bank. On the other hand, a very excessive LCR suggests that the bank has a lot of free funds, which do not work, and therefore do not generate income. Nevertheless, let us try to reflect the situation in the following table.

| Bank Name | Total Assets (30.06.21) | Liquid Assets (30.06.21) | Liquid Assets to Total Assets Ratio (30.06.21) % |

LCR (30.06.2022)

% |

| BCR Chisinau | 2827699,1 | 1756485,0 | 62,12 | 328,56 |

| Comertbank | 1891722,3 | 947965,4 | 50,11 | 326,19 |

| Energbank | 2971458,1 | 1920264,3 | 64,62 | 390,14 |

| Eurocreditbank | 1397896,3 | 715090,1 | 51,15 | 276,23 |

| Eximbank | 4539038,2 | 2583253,7 | 56,91 | 519,31 |

| Fincombank | 3984102,6 | 2143218,3 | 53,79 | 372,02 |

| maib | 33183256,3 | 14801381,6 | 44,60 | 139,23 |

| Moldindconbank | 22564650,3 | 12880090,7 | 57,08 | 304,27 |

| OTP Bank | 14945401,2 | 6385292,2 | 42,72 | 150,17 |

| ProCredit Bank | 4908057,6 | 1463756,2 | 29,82 | 390,26 |

| Victoriabank | 16478168,2 | 9140981,7 | 55,47 | 186,62 |

| Total | 109691450,2 | 54737779,2 | 49,90 | 307,50 |

According to the methodology used until early 2022, the minimum ratio of liquid assets should not be less than 20%. Going below this figure would indicate a bank's liquidity problems. On the other hand, if this ratio is too high, it means that the bank is certainly very liquid (solvent), but from the shareholders' point of view, it does not manage the assets competently enough. Increased liquidity suggests that most of the money does not work and does not generate profit.

According to the new methodology, which is already calculated as a percentage, the LCR should not be below 100%. In other words, all banks in the country as of June 30, 2022, are liquid three times the normalized level.

In 1H 2022, the banks increased the volume of attracted deposits relative to the same period last year. This was also facilitated by the increase in rates. If last year deposits in MDL were attracted at an average of 5% per annum, this year – at an average of almost three times higher - at 13%.

| Bank Name | Deposits Total (30.06.2022) | Deposits Total (30.06.2021) | Dynamics of Deposits (thousands of MDL) | Dynamics of Deposits (%) |

| BCR Chisinau | 2086355,6 | 2237186,6 | -150831,0 | -6,74 |

| Comertbank | 1329553,8 | 1196472,6 | 133081,2 | 11,12 |

| Energbank | 1938672,3 | 2131995,1 | -193322,8 | -9,07 |

| Eurocreditbank | 967975,8 | 996171,0 | -28195,2 | -2,83 |

| Eximbank | 3229700,1 | 3211866,2 | 17833,9 | 0,56 |

| Fincombank | 3113927,5 | 2890275,5 | 223652,0 | 7,74 |

| maib | 29335125,6 | 25574644,6 | 3760481,0 | 14,70 |

| Moldindconbank | 18301658,7 | 17250823,7 | 1050835,0 | 6,09 |

| OTP Bank | 12892525,6 | 11907208,8 | 985316,8 | 8,27 |

| ProCredit Bank | 2914472,9 | 2635711,0 | 278761,9 | 10,58 |

| Victoriabank | 12339779,9 | 12984113,8 | -644333,9 | -4,96 |

| Total | 88449747,8 | 83016468,9 | 5433278,9 | 6,54 |

Four banks showed a decrease in the volume of attracted deposits. On the whole, the growth in the system was 6.64%, with maib being the leader.

Attracting deposits in the banking system is divided into: individuals and legal entities. Usually, individuals are offered higher rates. At the same time, individuals carry higher risks in case of crisis situations, especially when accompanied by panic. With legal entities panic is usually not so pronounced, and can be "smoothed" with administrative resources from both the bank and the regulator - the NBM. That is why the more private deposits the bank has, the more it pays the yield on them and the more it risks in case of a possible panic. One of the main reasons for a possible panic in the banking market is a sharp devaluation of the national currency, when the depositors run to the bank to withdraw their MDL deposits in order to convert their savings into foreign currency. We saw such panic in particular in early 2015 after the disclosure of the "secret of the theft of the billion". It was "extinguished" quickly enough, although the MDL depreciated then.

Therefore, attracting deposits from legal entities for banks is considered not only more profitable, but also slightly less risky.

| Bank Name | Share of legal entities’ deposits (30.06.22) | Share of legal entities’ deposits (30.06.21) | Dynamics of legal entities share |

| BCR Chisinau | 58,10 | 56,09 | 2,01 |

| Comertbank | 36,98 | 27,64 | 9,34 |

| Energbank | 43,68 | 43,51 | 0,18 |

| Eurocreditbank | 34,15 | 29,35 | 4,80 |

| Eximbank | 52,71 | 45,73 | 6,98 |

| Fincombank | 43,34 | 37,55 | 5,79 |

| maib | 37,80 | 27,81 | 9,99 |

| Moldindconbank | 30,45 | 23,90 | 6,55 |

| OTP Bank | 46,66 | 41,86 | 4,79 |

| ProCredit Bank | 51,75 | 32,76 | 18,99 |

| Victoriabank | 39,14 | 41,51 | -2,36 |

| Total | 39,51 | 33,53 | 5,99 |

In H1 2022, compared to the same period of the previous year, Procredit Bank increased the share of legal entities’ deposits the most. Counting from the opposite, Moldindconbank has the largest share of individuals’ deposits.

In general, some bankers say they expect the loan portfolio to decrease by the end of 2022 and that the delays in payments on loans to start. There is also a pent-up demand for investment loans, even for those approved until February 2022. After quite a long period of low interest rates on loans, borrowers are psychologically not ready yet for higher interest rates on loans, especially when they will continue to grow.

Deposits might grow as well, though banks will hardly be interested in providing high interest rates on deposits under the current high liquidity and scarcity of opportunities and demand for further placement of funds. And they certainly will not cover the inflation rate.

Although the situation does not look rosy, as we have not yet overcome the peak of the recession, the banking system remains probably the most stable sector in Moldova. This stability, formed especially during the past eight years, was not easy, but without it the Moldovan economy would have had a hard time. And when the macroeconomic situation in the country hits the bottom, with a healthy circulatory system, the economy will have something to fall back on. //25.07.2022 - InfoMarket.